%20(1).png)

Your Journey Starts Here: Overcoming Credit Challenges

The Roadblock: Credit Rejection

Credit rejection can feel like a dead end, but it’s often the first step toward reshaping your financial future.

This guide will provide you with a clear roadmap to overcome credit challenges, empowering you to secure better financing opportunities, expand your trucking business, and achieve long-term financial stability.

By investing your time in this guide, you'll gain actionable strategies to rebuild your credit, unlock savings, and position yourself for success in the trucking industry.

Chapter 1

5 Ways Credit Drives Trucking Success

Many owner-operators believe that poor credit is just an obstacle they have to live with, but that mindset could be holding you back. Just because you've been denied financing before doesn’t mean you’re stuck.

The real challenge is understanding how much power your credit holds—and how to use it to your advantage. Without the right strategies, it’s easy to miss out on opportunities that could drive your business forward.

In this section, we’ll cover 5 ways your credit can fuel success: unlocking financing, enabling growth , and creating a competitive edge.

1. Financing Opportunity

Commercial Equipment Financing Requires Strong Credit

A healthy credit score is crucial for securing the funds needed to purchase or lease the equipment that drives your business forward.

Lenders Assess Credit Scores to Determine Loan Risk

Higher credit scores signal financial responsibility, increasing your chances of approval and access to competitive loan products.

2. Loan Repayment Savings

Higher Scores Unlock Better Interest Rates & Terms

A strong credit profile can reduce overall borrowing costs, saving your business thousands over the lifespan of a loan.

Potential Savings: $10,000-$50,000 Over Loan Lifetime

A strong credit profile can reduce overall borrowing costs, saving your business thousands over the lifespan of a loan.

3. Exclusive Financing Perks

Faster Approval Processes

Save valuable time when applying for loans, enabling quicker decision-making and execution.

Financing Programs for High-Credit Businesses

High credit scores qualify you for unique programs offering flexible terms and rates unavailable to others.

4. Competitive Advantage

Better Credit Means Better Terms, More Opportunities

Stand out from competitors by securing favorable agreements and optimizing costs.

Unlock Premium Insurance Rates

Reduce overhead costs by qualifying for lower premiums tied to strong credit scores.

Access to Larger Equipment Loans

Build your fleet with confidence, knowing you have the financial backing to expand without setbacks.

5. Build Trust, Gain Partners

Positioning Your Business as Financially Stable

Demonstrate to stakeholders that your business is built on a solid credit-backed foundation.

Attract Potential Business Partners

A strong financial foundation signals reliability, making you a preferred choice for partnerships.

Chapter 2

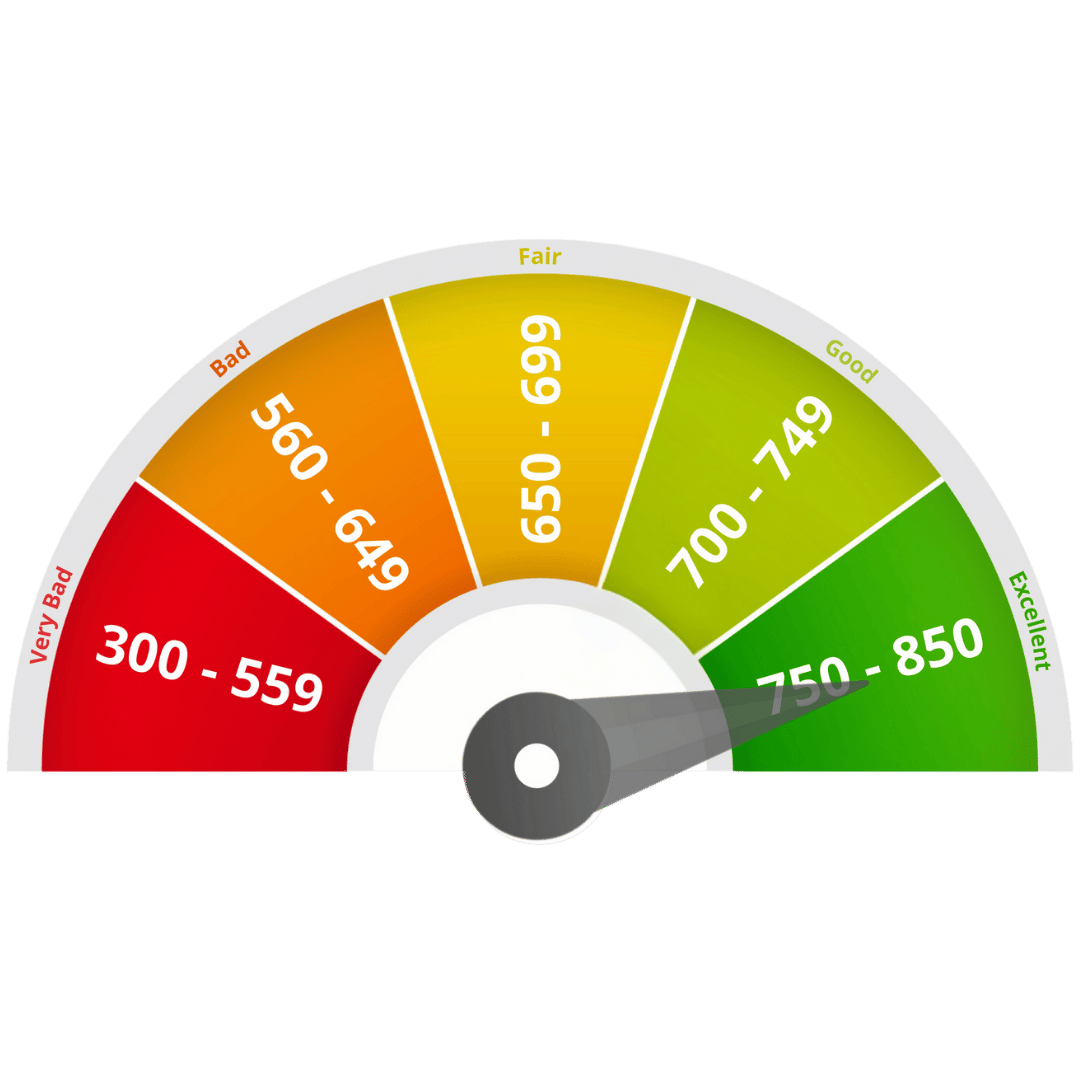

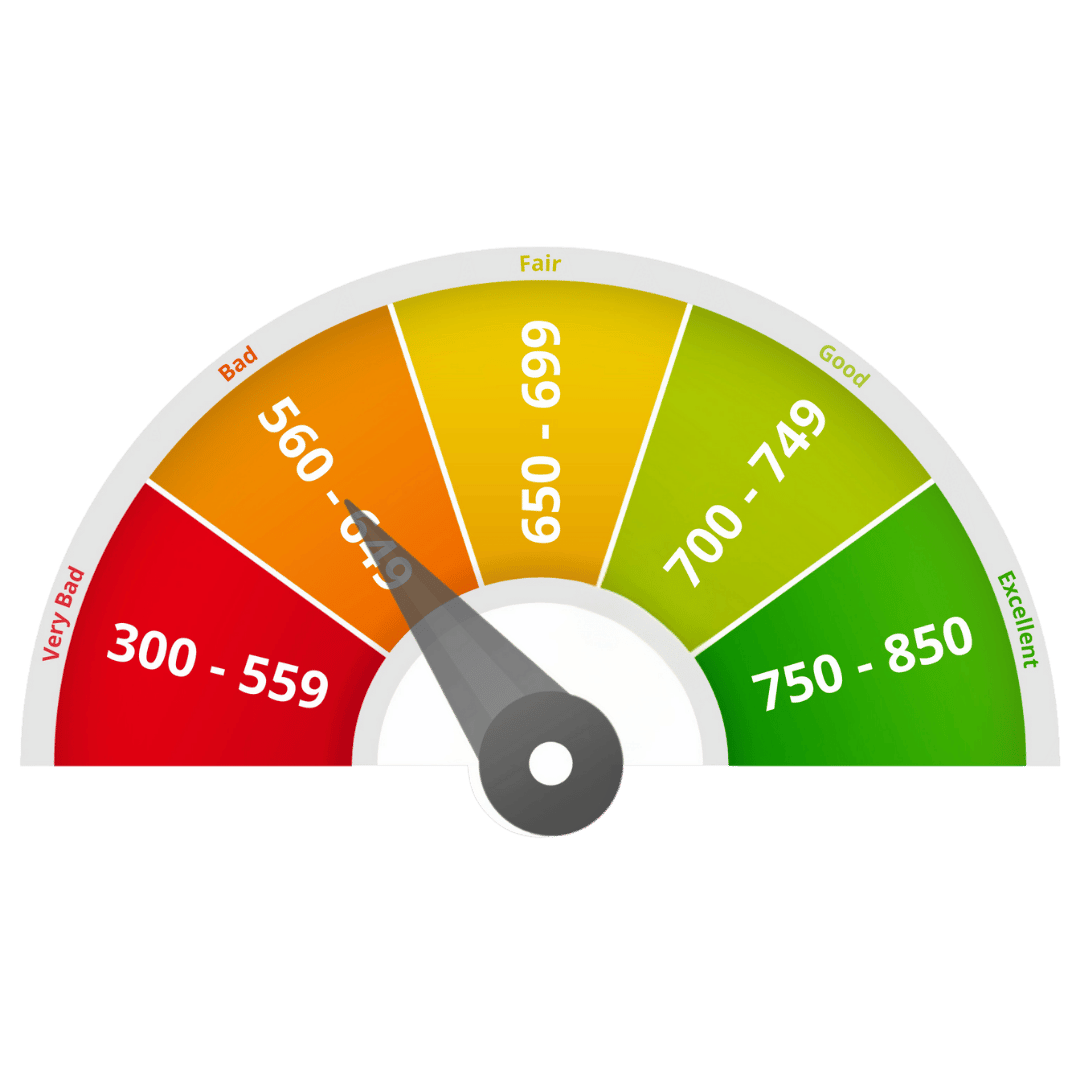

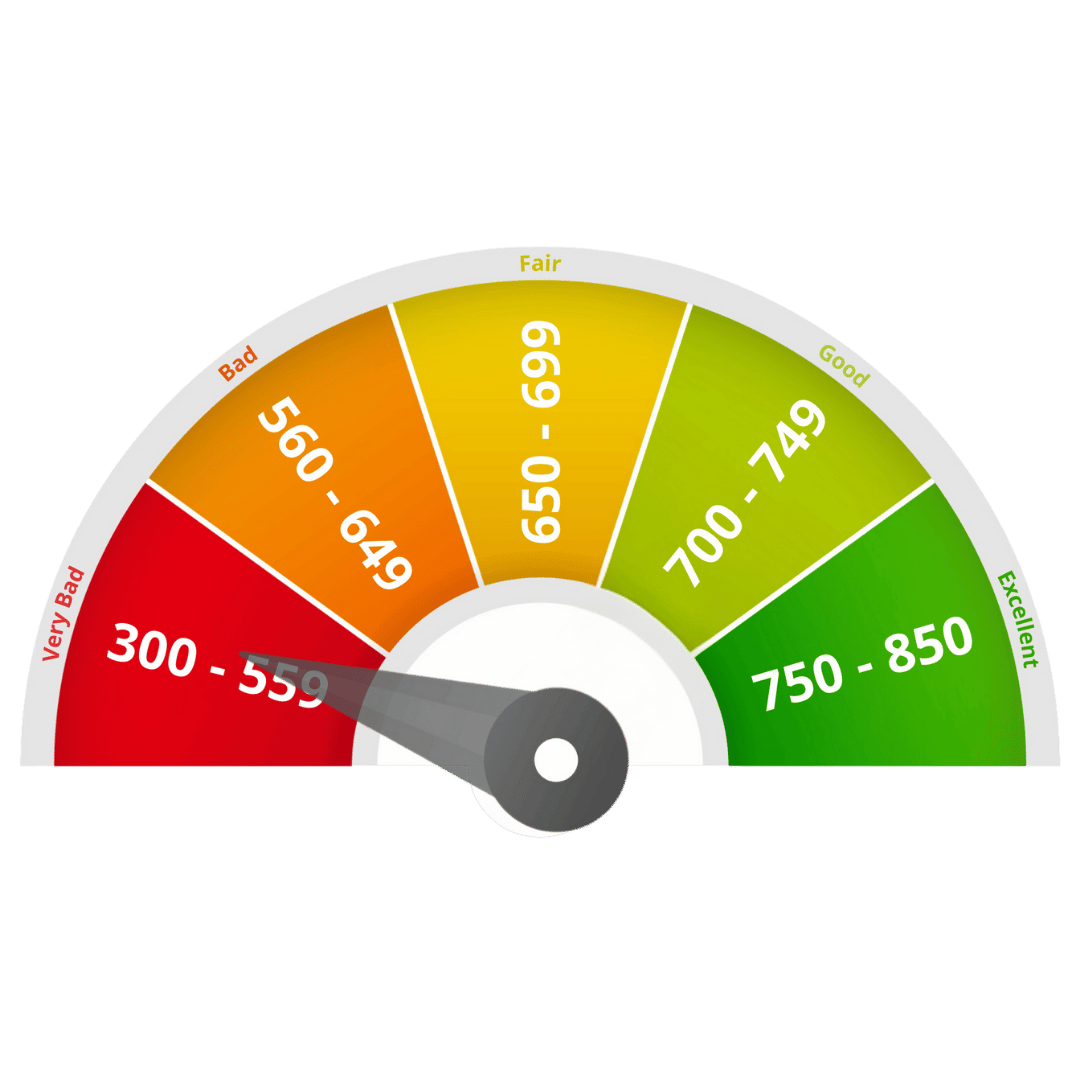

Understanding Your Credit Landscape

A credit score isn't just a number—it's a financial tool that opens doors or creates hurdles, depending on where you stand. In trucking, your credit score determines not only your ability to secure financing but also the rates, terms, and opportunities available to your business.

In this chapter, we’ll break down the different credit score ranges and what they mean for your ability to finance your trucking business. You’ll learn where you stand, what opportunities are available to you, and how to shift your score into the range that opens the best doors for your future.

Excellent: 750-850

Welcome to the credit score hall of fame! In this tier, you’re practically a lender’s dream. Expect the best of the best: rock-bottom interest rates, near-instant approvals, and access to premium financing options.

With this kind of flexibility, you’re not just buying equipment—you’re making strategic moves for your trucking empire. Keep it up, and you’ll continue to see doors swing wide open for every opportunity.

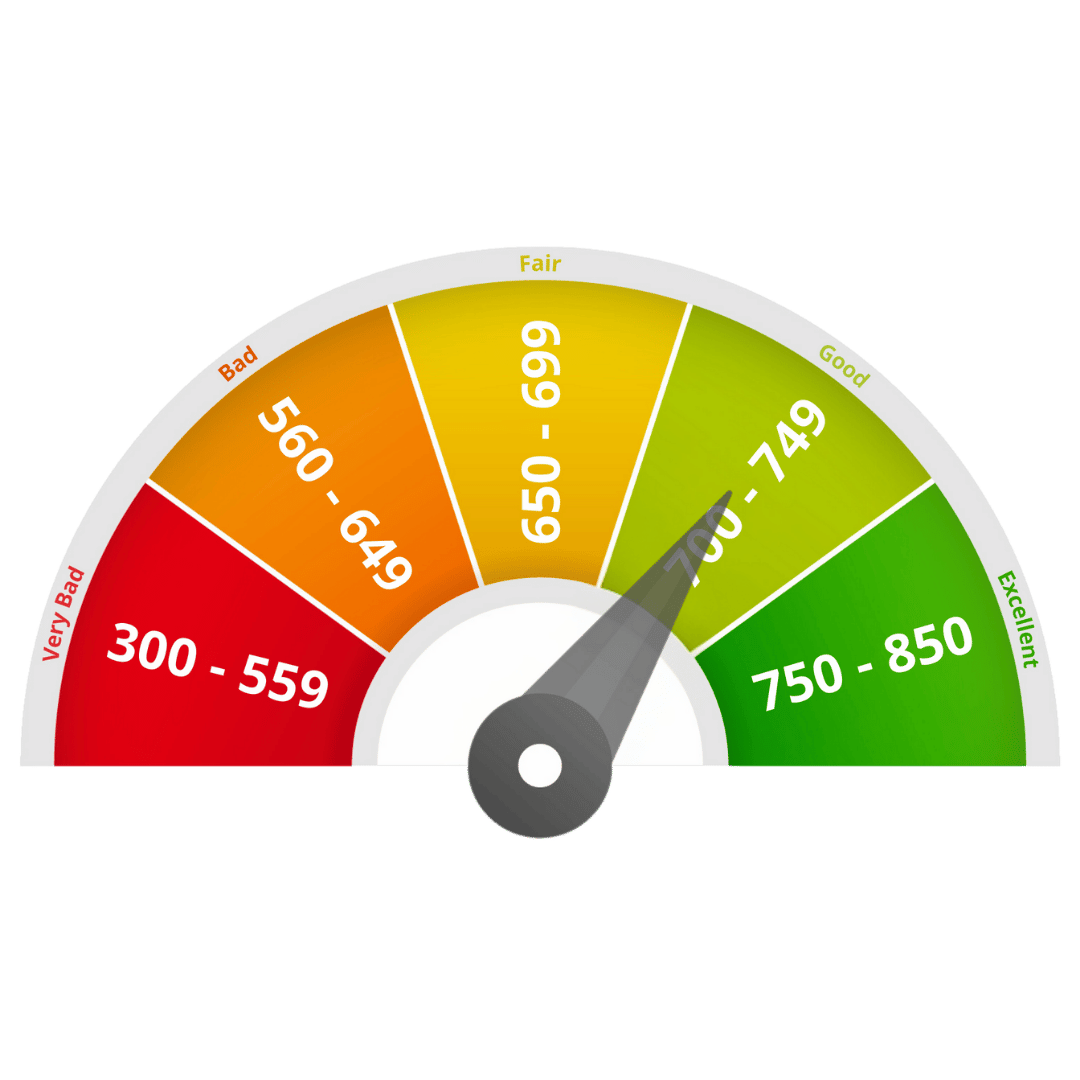

Good: 700-749

You’re in a solid spot here—no need to stress. Lenders still love you, and you can secure great interest rates and financing terms.

Sure, you might not get the absolute lowest rates out there, but you’re well within the range to grow your trucking business without hitting major roadblocks.

A few smart financial moves could bump you into the “excellent” range and unlock even more perks.

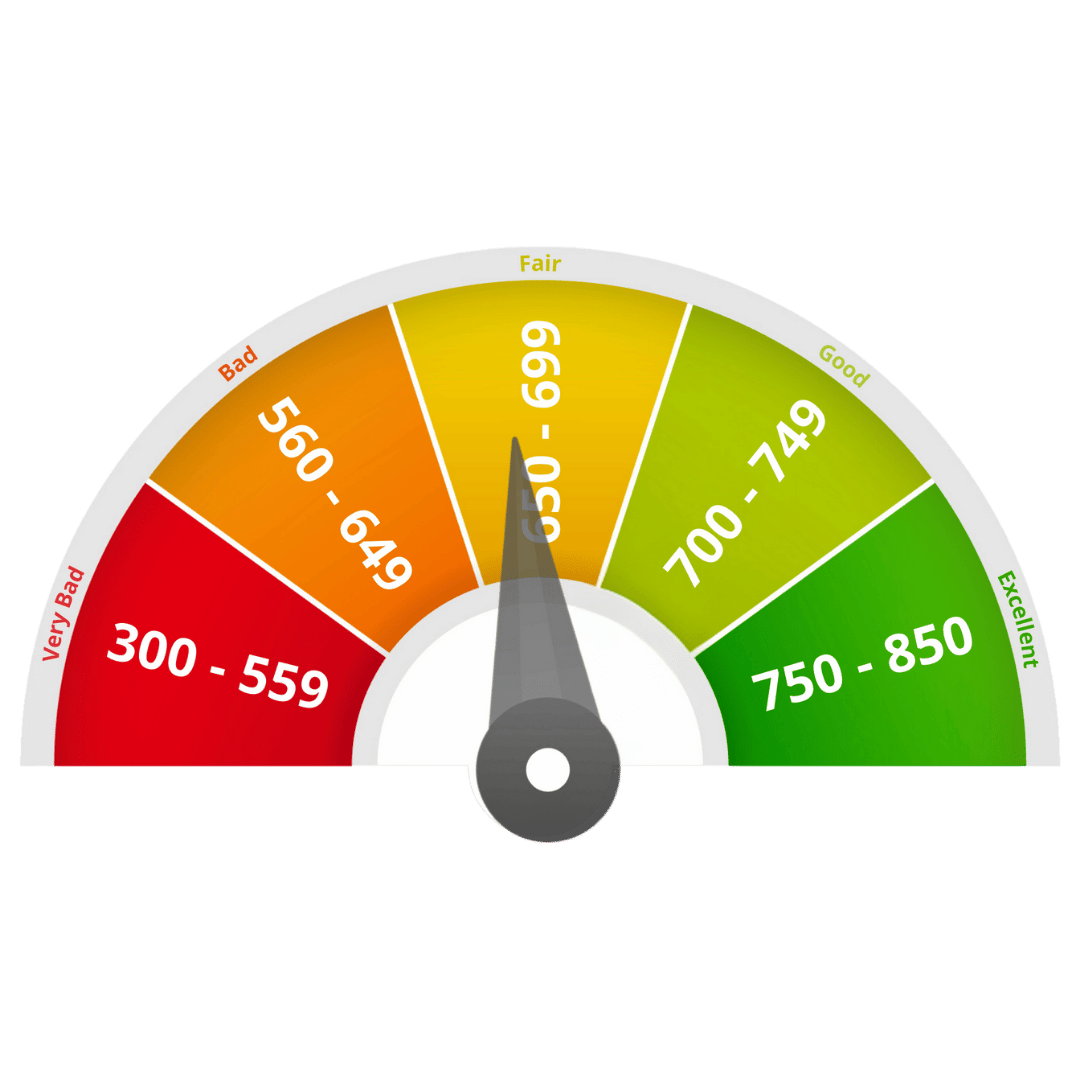

Fair: 650-699

Here’s where things start to get a little bumpy. You can still get financing, but expect lenders to ask for extra paperwork and tack on higher interest rates.

It’s like driving uphill: you can make it, but it takes more effort. The good news? With some strategic credit-building—like paying down debt and making on-time payments—you could quickly climb to the next level.

Poor: 560-649

You’re in the “red zone,” but don’t panic—it’s not the end of the road. Lenders might be cautious, and you’ll face steep interest rates, but there are still options.

Collateral or specialized programs can help you secure funding when you need it most. Think of this as a wake-up call: now’s the time to prioritize your credit repair efforts and start turning things around.

Critical: Below 560

This is the “pull over and assess” range. Financing at this level is tough, and lenders will likely require a cosigner or substantial collateral.

But don’t let that discourage you—your credit score isn’t a life sentence. This guide is packed with strategies to help you repair your credit, rebuild trust with lenders, and work your way toward financial freedom. You’ve got this!

Chapter 3

Common Credit Challenges in Trucking

Navigating the trucking industry requires financial stability, but many owner-operators and trucking companies face credit-related obstacles that can hinder their progress. From managing debt to rebuilding after financial setbacks, these challenges often feel overwhelming but are far from insurmountable.

Understanding these common issues and the strategies to address them can pave the way for better creditworthiness and financial growth in trucking. In this chapter we’ll take a closer look at the most frequent credit challenges and how they impact the industry.

High Debt-to-Income Ratio

A high debt-to-income ratio signals to lenders that your income may not comfortably cover your debt obligations. This challenge can result in limited financing options or higher interest rates.

Trucking businesses often face this issue due to the significant costs of equipment, fuel, and maintenance. Debt consolidation strategies, such as combining multiple loans into one manageable payment, can help reduce financial strain and free up cash flow for operational needs.

Late Payment History

Late payments are a red flag to creditors, as they indicate unreliability in meeting financial obligations. Over time, this damages credit scores and limits financing options.

In trucking, inconsistent cash flow caused by delayed payments from clients can exacerbate this issue. Rebuilding trust with creditors requires consistent on-time payments and proactive communication to negotiate more favorable terms when needed.

Limited Credit History

Entrepreneurs in the trucking industry with shorter credit histories may find it harder to secure financing or competitive loan terms. Lenders often view limited credit as a lack of demonstrated reliability.

However, using alternative verification methods, such as income records or operational performance, can strengthen your case. Gradually building credit with small, manageable loans and timely payments can also improve your financial profile over time.

Previous Financial Setbacks

Financial setbacks like bankruptcy or repossession can leave a lasting mark on creditworthiness, making future financing more challenging. While recovery takes time, it is possible with focused effort.

Specialized programs designed for post-bankruptcy recovery, combined with a disciplined approach to budgeting and debt repayment, can help trucking businesses rebuild their financial standing and regain access to necessary funding.

Chapter 4

Your 5-Step Credit Repair Blueprint

Repairing credit can feel like an overwhelming task, but breaking it into manageable steps transforms the process into a clear and achievable goal.

This blueprint focuses on practical, effective strategies to address common credit issues, correct errors, and build a strong financial foundation.

Whether you're just starting or already on the road to recovery, these steps are designed to guide you toward credit improvement and long-term stability

Step 1: Credit Assessment

The foundation of any credit repair journey begins with understanding your credit report and identifying areas for improvement.

✦ Identify negative items:

A detailed review of your credit report ensures every negative entry is accounted for, providing a clear roadmap for action.

✦ Understand your starting point:

Establishing your baseline credit score and setting realistic goals helps you measure progress and stay motivated.

Step 2: Error Correction

Inaccuracies on your credit report can unfairly drag down your score, making this step critical for quick improvements.

✦ Dispute inaccurate negative entries:

Leveraging your consumer rights, you can challenge errors and clean up your credit report using proven techniques.

✦ Request verification of debt:

Verify all claims against you to ensure they’re legitimate and challenge anything that lacks proper documentation.

Step 3: Debt Management

Effective debt management reduces financial stress and accelerates credit repair by optimizing your repayment approach.

✦ Negotiate with creditors:

Skilled negotiations can result in reduced interest rates, more manageable repayment terms, or even partial debt forgiveness.

Step 4: Credit Rebuilding

Demonstrating financial responsibility is key to improving your creditworthiness over time.

✦ Secure a credit-builder credit card:

These cards provide a low-risk way to rebuild credit with manageable limits and consistent on-time payments.

✦ Become an authorized user on a strong account:

Partnering with someone who has excellent credit history can give your score an immediate boost.

Step 5: Ongoing Monitoring

Credit repair doesn’t stop once your score improves. Ongoing monitoring ensures you catch potential issues early and maintain your progress.

✦ Utilize credit monitoring services:

Real-time alerts help you respond to changes quickly, keeping your credit profile secure and stable.

.jpg)

Congratulations on Making it to the End!

You’ve just completed the ultimate guide to credit repair in the trucking industry—making you one of the most informed professionals on the road to financial success!

Ready to take the next step?

Download our exclusive Credit Repair Kit, packed with over 100 actionable dispute templates and a step-by-step guide to help you repair your credit and unlock new opportunities.

Don’t just stop here—put your knowledge into action and drive toward a brighter financial future!