The Car Buyer’s Credit Repair Guide

Drive Your Future Forward & Secure Your Auto Loan

Your Path to a New Vehicle Starts Here

Repairing Your Credit for Auto Financing Approval

Being denied an auto loan can feel like a dead end, but it’s really just the starting point of your financial comeback. Your credit score isn’t just a number—it’s a key that unlocks better car loan approvals, lower interest rates, and financial freedom.

If you’re looking to repair your credit to get approved for an auto loan, you’re in the right place. This guide will show you step-by-step strategies to rebuild your credit, increase your loan approval chances, and save thousands on your next car purchase.

Chapter 1

The Power of a Strong Credit Score for an Auto Loan

Many car buyers don’t realize just how much their credit affects their ability to buy a vehicle. Let’s break down exactly how your credit score plays a role in your auto loan—and how you can take control of it.

Your credit score impacts:

Loan Approvals

Higher scores mean higher approval chances.

Monthly Payments

A good score keeps your payments affordable.

Interest Rates

Total Interest Cost

A lower rate means less interest paid over time.

Chapter 2

How Your Credit Score Affects Interest Rates & Total Loan Costs

Your credit score directly impacts the interest rate lenders offer you. A higher score means a lower interest rate, saving you money in the long run.

Here’s what that looks like for a $15,000 auto loan over a 60-month term:Credit

| Credit Score | Estimated Interest Rate | Monthly Payment | Total Interest Paid | Total Loan Cost |

|---|---|---|---|---|

| 750+ | 4.5% | $280 | $1,775 | $16,775 |

| 700-749 | 6.5% | $293 | $2,570 | $17,570 |

| 650-699 | 9.5% | $314 | $3,835 | $18,835 |

| 600-649 | 14.0% | $349 | $5,905 | $20,905 |

| Below 600 | 21.0% | $407 | $9,370 | $24,370 |

The difference between an excellent and a poor credit score could mean paying over $4,000 more in interest—or even $7,500 more if your score is below 600. That’s money that could stay in your pocket with the right credit repair strategy.

The Long-Term Impact: Your Credit & Loan Amortization

Your credit score doesn’t just affect your monthly payments—it affects your amortization schedule, or how much you pay toward interest vs. principal over time.

For example, let’s say you finance a $15,000 car over 5 years:

- With a 750+ score at 4.5%, you pay about $1,775 in interest.

- With a 600 score at 14%, you pay nearly $5,905 in interest.

That’s over $4,000 in extra costs just because of a lower credit score!

But here’s something most borrowers don’t realize: interest is front-loaded in most auto loans.

That means in the early years of your loan, the majority of your payment goes toward interest rather than reducing your principal. If your credit score forces you into a high-interest loan, you’ll stay underwater—owing more than your car is worth—for much longer. This makes it harder to refinance or sell the vehicle without taking a financial hit.

A strong credit score doesn’t just lower your interest rate—it helps you build equity in your vehicle faster, giving you more financial flexibility down the road.

Chapter 3

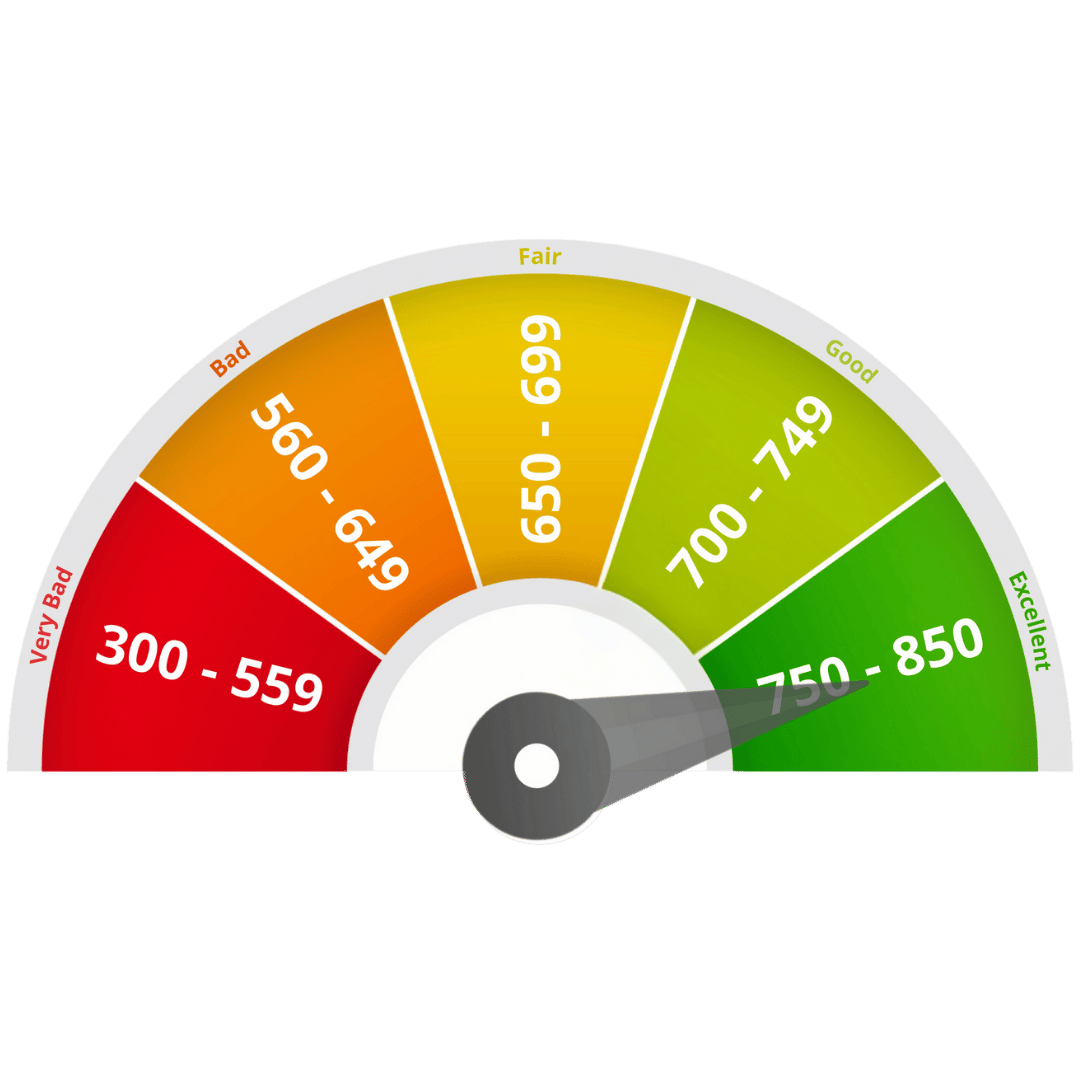

Understanding Your Credit Score & Loan Approvals

Your credit score can either be the key to unlocking favorable auto loan rates, terms, and opportunities, or the hurdle that keeps your dream car just out of reach.

In this chapter, we’ll decode the different credit score ranges, revealing what each means for securing financing for your vehicle.

Discover:

- Where You Stand: Understand your current credit score’s implications.

- Available Opportunities: Learn which auto loan options are within your grasp.

- Path to Improvement: Get insights on how to enhance your score, unlocking better financial possibilities for your next car purchase.

Excellent: 750-850

- Best interest rates

- Easy approval

- More vehicle choices

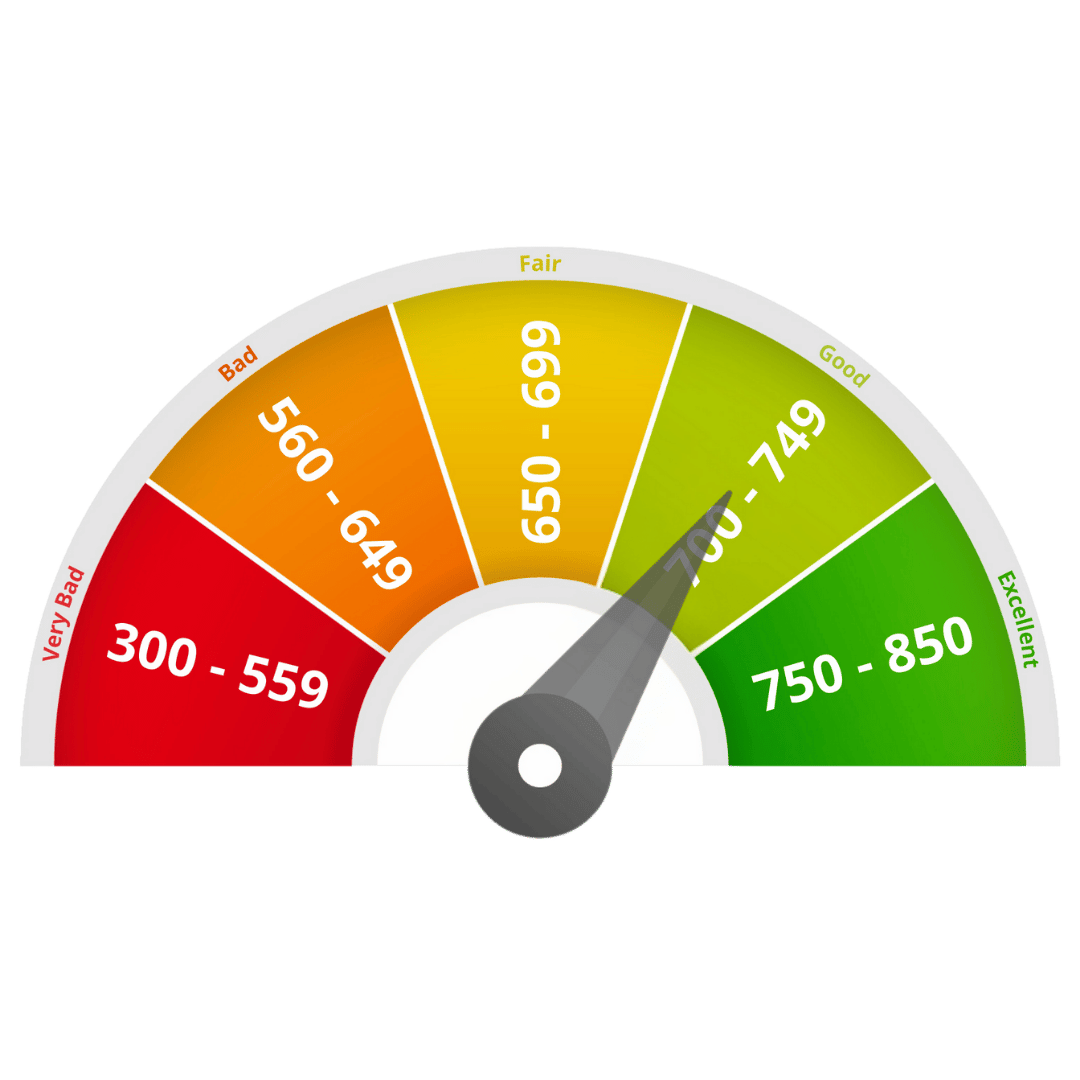

Good: 700-749

Solid Drivetrain: You're in a great spot! Lenders view you favorably, offering:- Competitive interest rates & terms

- Strong approval odds

- Affordable monthly payments

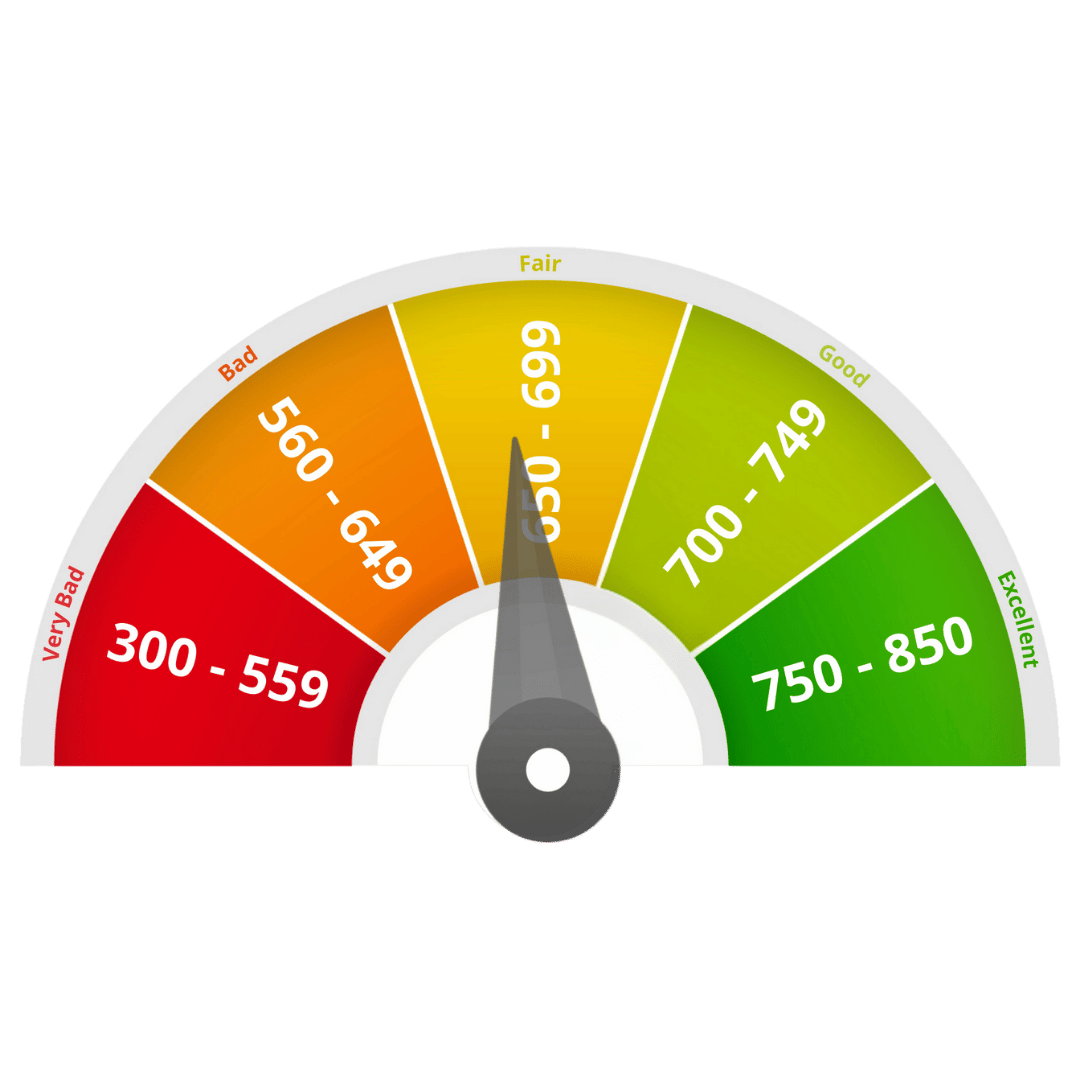

Fair: 650-699

Room for Improvement: You can still get approved for an auto loan, but:- Expect higher interest rates

- Be prepared for a higher down payment

- You may have access to fewer financing options

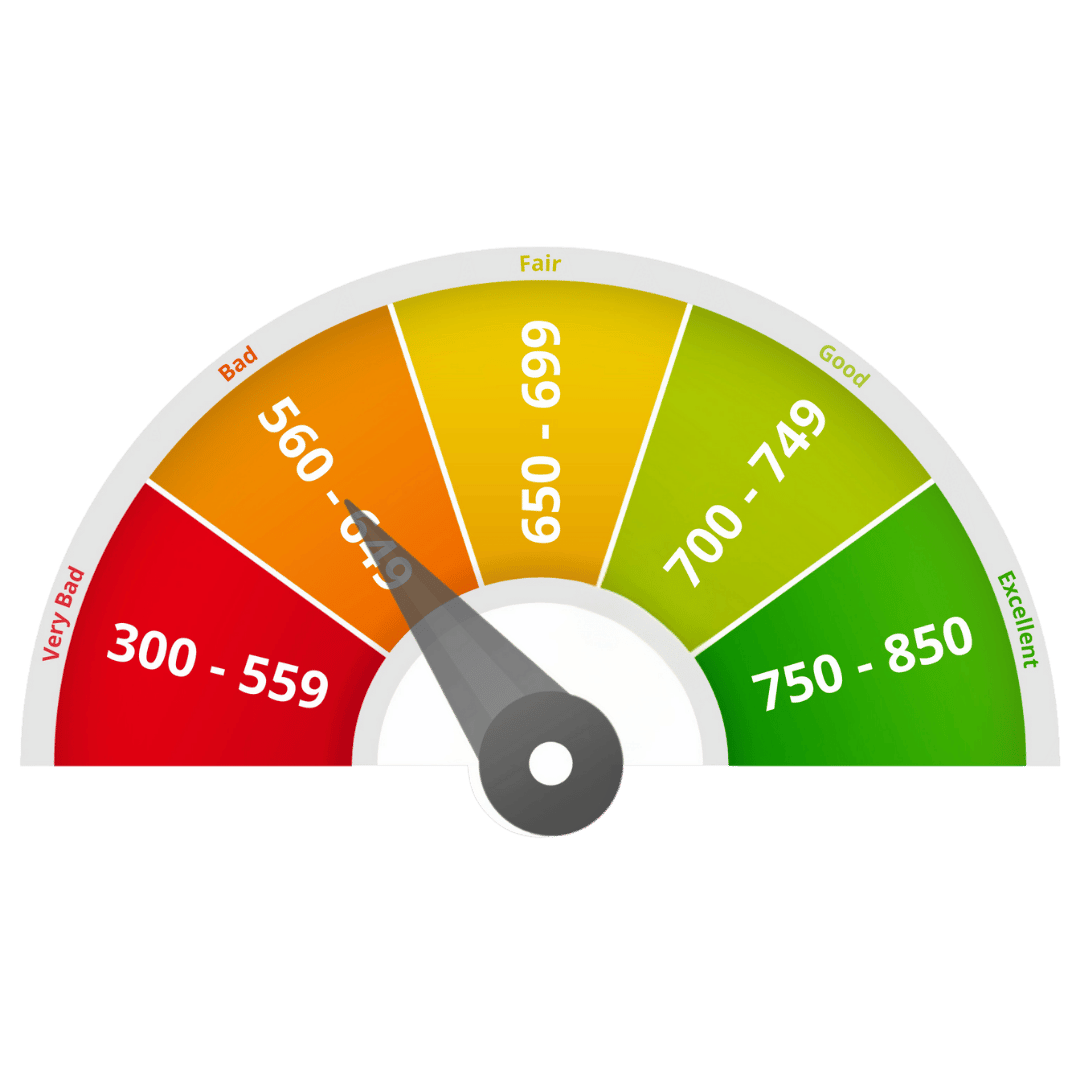

Poor: 560-649

Time to Refocus: You're facing challenges, but don't worry, it's not a dead end. Be prepared for:- Very high interest rates

- Challenging loan approval process

- Often requires a cosigner

Use this as a motivation to prioritize credit repair and get back on track!

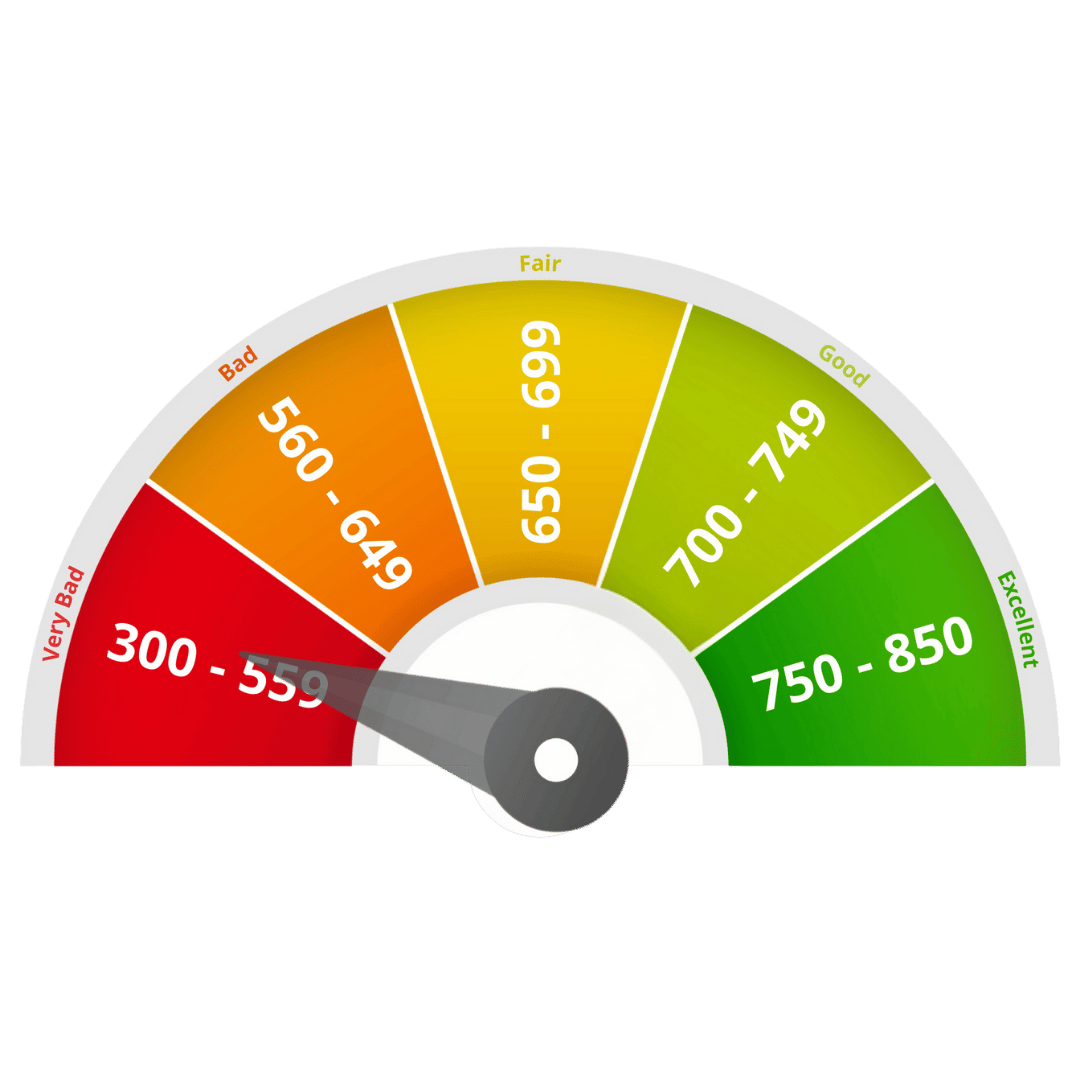

Critical: Below 560

Take a Breath, Reassess: Financing might be tough, you'll be denied by most lenders. The lenders do offer financing may require:- Subprime financing with extreme interest rates

- Substantial collateral

- A cosigner

- Learn from our credit repair strategies

- Rebuild trust with lenders

- Work towards financial freedom and your dream home. You've got this!

Chapter 4

5 Steps to Rebuild Your Credit & Get Approved

Step 1: Check Your Credit Report for Errors

- Incorrect late payments

- Accounts that aren’t yours

- Outdated negative marks

Dispute any errors with the credit bureaus to ensure your score reflects accurate information.

Step 2: Pay Down Existing Debt

Lowering your credit utilization (the amount of credit you use vs. your limit) can quickly boost your score. Focus on paying off credit cards and loans with high balances.

Step 3: Make On-Time Payments—Every Time

Payment history is the biggest factor in your credit score. Set up autopay or reminders to ensure you never miss a due date.

Step 4: Consider a Credit-Builder Loan or Secured Credit Card

If you have little or poor credit history, a credit-builder loan or secured credit card can help you establish a positive payment history.

Step 5: Avoid New Hard Inquiries

Each time you apply for a loan, the lender performs a “hard inquiry” that can temporarily lower your score. Only apply when you’re confident you’ll be approved.

Congratulations on Making it to the End!

Your dream car is within reach. The key to approval—and securing a great rate—is improving your credit score. By following these steps, you can:

✅ Secure a better loan with lower rates

✅ Reduce your monthly car payment

✅ Save thousands over the life of your loan

Start today! Check your credit, make a plan, and get back on the road with confidence.